Renters insurance doesn’t cost much, but it can save you thousands of dollars if your belongings suffer accidental damage at home. We collected dozens of quotes and evaluated five top Wisconsin insurers to find the best, most affordable option in the state.

The best price for renters insurance in Wisconsin is $11 per month, but we don’t recommend buying coverage based on price alone. Coverage options and customer service are equally important.

Best renters insurance for most people: State Farm

State Farm has the best overall mix of affordable prices, dependable customer service and useful optional coverages.

Read our full review of State Farm insurance

The good:

- Lowest prices in the state

- Well-rated customer service

The bad:

- Not as many useful extra coverage options

State Farm is our recommendation for most renters insurance shoppers in Wisconsin. It had the lowest prices of any company we looked at, plus solid customer service ratings and good coverage options.

The average price we found from State Farm was $11 per month. That’s 30% lower than average among all the insurers we considered and 44% lower than the most expensive rate we found.

Customer service from State Farm is great, too. State Farm has a Complaint Index of 0.38 from the National Association of Insurance Commissioners (NAIC). This means it received just 38% as many complaints as a typical insurer and suggests that customers were usually satisfied with their service. J.D. Power also gave it a score of 850/1,000 in its renters insurance satisfaction survey, which was among the best ratings of any insurer nationwide.

The only relative downside to State Farm is that its coverage options are good, but not great. It has some useful optional coverages, like valuable items coverage and extended liability; however, it’s lacking in others we think may be beneficial to some renters, such as replacement cost coverage and equipment breakdown.

Best coverage options: Travelers

Travelers has the best selection of coverage options for Wisconsin renters.

Read our full review of Travelers.

The good:

- Lots of useful optional coverages

The bad:

- Higher-than-average rates

- Must buy the policy in annual installments

For renters who have very particular coverage needs that our top pick can’t meet, we recommend Travelers Insurance. That company had the best overall selection of optional coverages we found in Wisconsin.

There are a lot of options to choose from at Travelers. You can add equipment breakdown coverage, which pays for the cost to repair an appliance that stops working, as well as valuable items coverage and replacement cost coverage.

However, Travelers’ rates are above average — even without the extra coverages added on. We found a typical price of about $16 per month, which is just slightly above average among the insurers we considered. And any optional coverages you include will raise your rate even more.

Frustratingly, Travelers also requires you to pay your bill in annual installments, rather than on a monthly basis. That means that instead of paying about $16 once a month, you have to pay $186 once per year. While the net cost works out to be only slightly higher than other companies we looked at, the larger one-time payment may make it a more difficult burden for some renters.

Customer service from Travelers is also only mediocre. It has a Complaint Index from the NAIC of 0.50. While that means it received only half as many complaints as a typical insurer nationwide, it’s significantly worse than State Farm’s score. And J.D. Power gave it a 796 rating out of 1,000, which also doesn’t measure up to State Farm.

Runner-up for low prices: Allstate

Allstate’s prices were almost as affordable as what we found at our top pick.

Read our full review of Allstate.

The good:

- Rates are almost as affordable as our top pick’s

The bad:

- Mediocre coverage and service

For renters focused on affordability who can’t get a good rate from State Farm, we recommend Allstate. Its prices were almost as competitive as our top pick’s, though its service and coverage options aren’t as strong.

The average rate we found at Allstate was about $13 per month. That’s 14% lower than the typical rate statewide, though $2 per month higher than our top pick.

Unfortunately, price is the main benefit of going with Allstate. It has middle-of-the-road customer service, with a 0.51 Complaint Index from the NAIC. That’s worse than either of our two top picks.

Coverage options from Allstate are similarly lackluster. It only offers two optional choices beyond the basics, neither of which are particularly rare or useful: identity theft coverage and extended liability coverage. Both of these are readily available at other insurers, though State Farm lacks identity theft.

How we chose the best renters insurance companies in Wisconsin

When evaluating the best Wisconsin renters insurance companies, we considered three key factors: affordability, coverage options and customer service.

- Affordability: Are the rates the insurer charges competitive with other local insurers?

- Coverage options: Does the insurer have a good mix of coverage options?

- Customer service: Are customers usually satisfied with the service they receive?

Affordability: Finding cheap renters insurance in Wisconsin

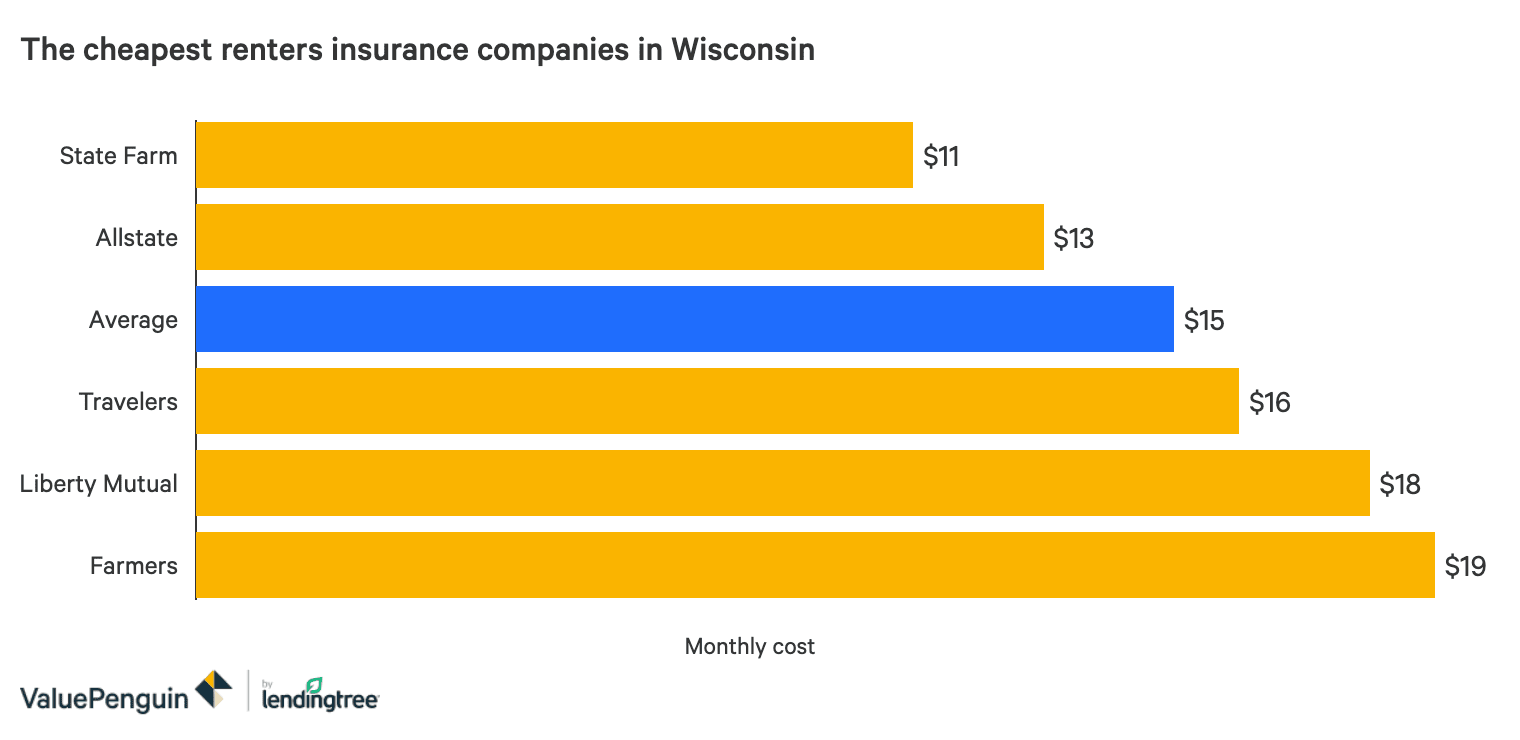

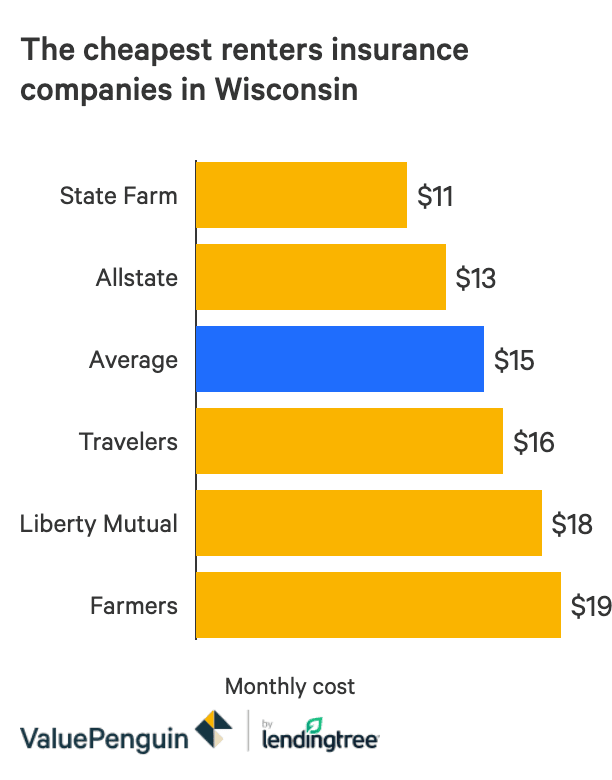

The average price we found for renters insurance in Wisconsin was $15 per month, though some insurers were cheaper than others. State Farm offered a price of just $11, a rate 44% cheaper than the most expensive option we found. Over the course of a year, that adds up to a savings of $98.

Here’s our full breakdown of the cheapest renters insurance companies in Wisconsin:

| Insurer |

Monthly cost |

% difference from average |

| Average |

$15 |

— |

| State Farm |

$11 |

-30% |

| Allstate |

$13 |

-14% |

| Travelers |

$16 |

2% |

| Liberty Mutual |

$18 |

19% |

| Farmers |

$19 |

23% |

Our selected levels of coverage were:

- Personal property coverage: $30,000

- Liability coverage: $100,000

- Medical payments coverage: $1,000

- Deductible: $500

- Loss of use: $0

Coverage options: Comparing renters insurance policies and benefits

No two renters have the same coverage needs: Some people might want extra protection for valuables, while others may benefit from equipment breakdown coverage. So when we evaluated optional coverages, we looked for companies that provide a wide range of useful coverage options.

Some especially useful options for Wisconsin renters include:

- Replacement cost coverage: Pays for the full cost to replace a destroyed or stolen item, without factoring in depreciation.

- Valuable/scheduled items coverage: Boosts coverage for expensive or valuable items you own, like jewelry, electronics or musical instruments, which may have limited coverage under a standard policy.

- Mechanical breakdown coverage: Pays to repair appliances and other equipment that malfunctions due to normal use.

- Water backup coverage: Pays for damage to property due to water backup.

In addition, every insurer we looked at offered all of the following basic protections. If you’re looking at an insurer that is missing any of these, consider that a red flag and look for another insurer instead.

- Personal property coverage: Pays to repair or replace items that are damaged, stolen or destroyed from a covered peril.

- Additional living expenses: Pays for a hotel or other temporary living arrangement if your home is uninhabitable due to a covered peril.

- Liability coverage: Pays monetary damages to others that you’re responsible for, such as if your dog injures a guest.

- Medical payments coverage: Pays for medical care of guests who are injured at your home, regardless of who is at fault. Pays out before liability coverage goes into effect.

Customer service: Evaluating insurer quality in service and claims

Picking a renters insurance company with strong customer service is essential, especially when you’re buying a policy or making a claim. An insurer with good customer service will be there to answer questions and resolve issues, while one without it will have frustrating delays.

To evaluate customer service among Wisconsin renters insurance companies, we considered three main sources of information: the National Association of Insurance Commissioners’ Complaint Index, J.D. Power’s renters insurance satisfaction survey and AM Best’s Financial Strength Rating.

| Insurer |

NAIC Complaint Index |

J.D. Power rating |

AM Best FSR |

| Allstate |

0.51 |

814 |

A+ |

| Farmers |

0.37 |

808 |

A |

| Liberty Mutual |

0.66 |

792 |

A |

| State Farm |

0.38 |

850 |

A++ |

| Travelers |

0.50 |

796 |

A++ |

What each rating means

- NAIC Complaint Index: This number compares the number of complaints an insurer has received to its size. A smaller number indicates fewer complaints and suggests that renters are more likely to be satisfied with their insurer. The national average is 1.00.

- J.D. Power ratings: This score is based on J.D. Power’s national renters insurance satisfaction survey. Ratings are on a 1,000-point scale, and a higher number indicates greater overall satisfaction. The national average score is 831.

- AM Best FSR: This letter grade evaluates an insurer’s overall financial health. Grades range from A++ to D, and a higher grade indicates that the company has a better ability to pay claims, even in times of high claim demand (like after a natural disaster) or economic downturn.

Wisconsin renters insurance: Costs by city

What you’ll pay for renters insurance can change based on where you live. Renters who live in areas with low crime might pay less, while renters who live far from a fire department might pay more. Here’s our city-by-city renters insurance breakdown for Wisconsin.

| City |

Average cost |

% difference from average |

| State average |

$15 |

— |

| Milwaukee |

$18 |

16% |

| Madison |

$16 |

4% |

| Green Bay |

$16 |

2% |

| Kenosha |

$18 |

17% |

| Racine |

$16 |

7% |

| Eau Claire |

$15 |

-2% |

| West Allis |

$16 |

4% |

| Waukesha |

$15 |

-1% |

| Oshkosh |

$14 |

-7% |

| La Crosse |

$15 |

1% |

| Appleton |

$14 |

-7% |

| Janesville |

$15 |

-2% |

| Sheboygan |

$15 |

-4% |

| Wauwatosa |

$16 |

5% |

| Fond du Lac |

$14 |

-6% |

| Greenfield |

$15 |

0% |

| Wausau |

$15 |

0% |

| Oak Creek |

$15 |

-1% |

| Beloit |

$15 |

-2% |

| Fitchburg |

$15 |

-3% |

| Sun Prairie |

$14 |

-6% |

| Stevens Point |

$14 |

-4% |

| Manitowoc |

$14 |

-7% |

| Superior |

$15 |

2% |

| West Bend |

$15 |

-4% |

Renters insurance costs change depending on what state you live in, too. To see how the cost of renters insurance varies by state, see our national study of renters insurance costs.

Methodology

To find the best renters insurance companies in Wisconsin, we evaluated five top insurers and gathered quotes for 25 cities across the state. All quotes are based on a sample renter profile of a 30-year-old man who lives alone and has no recent renters claims. He’s protected himself with $30,000 of personal property coverage with a $500 deductible, plus $500,000 of liability protection.